Some investment professionals work hard to make their work confusing. They believe they have a vested interest in creating investor confusion. They use jargon that can intimidate and make it difficult for you to understand relatively straightforward concepts.

But investing is actually not that complicated. We’ll explore three different methods that investors use to make decisions about their money, and we’ll talk about where you should be with your own approach to your portfolio.

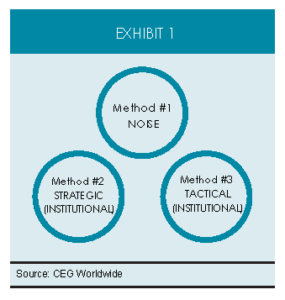

Exhibit 1 classifies people according to how they make investing decisions. The first method is the noise method. It’s used by investors who get caught up in the noise of the day and let their emotions dictate their actions. They chase after hot stocks and market sectors that are due to fall, ignore investments that are undervalued and poised to rise and, as a result, often earn poor returns that fail to get them to their most important financial goals.

Exhibit 1 classifies people according to how they make investing decisions. The first method is the noise method. It’s used by investors who get caught up in the noise of the day and let their emotions dictate their actions. They chase after hot stocks and market sectors that are due to fall, ignore investments that are undervalued and poised to rise and, as a result, often earn poor returns that fail to get them to their most important financial goals.

Unfortunately, it’s easy to get caught up in all the noise that’s out there. Most of the public uses the noise method, and much of the financial media fuels this method of investing as it tries to sell newspapers, magazines and television shows. For the media, it’s all about getting you to return to them time and time again.

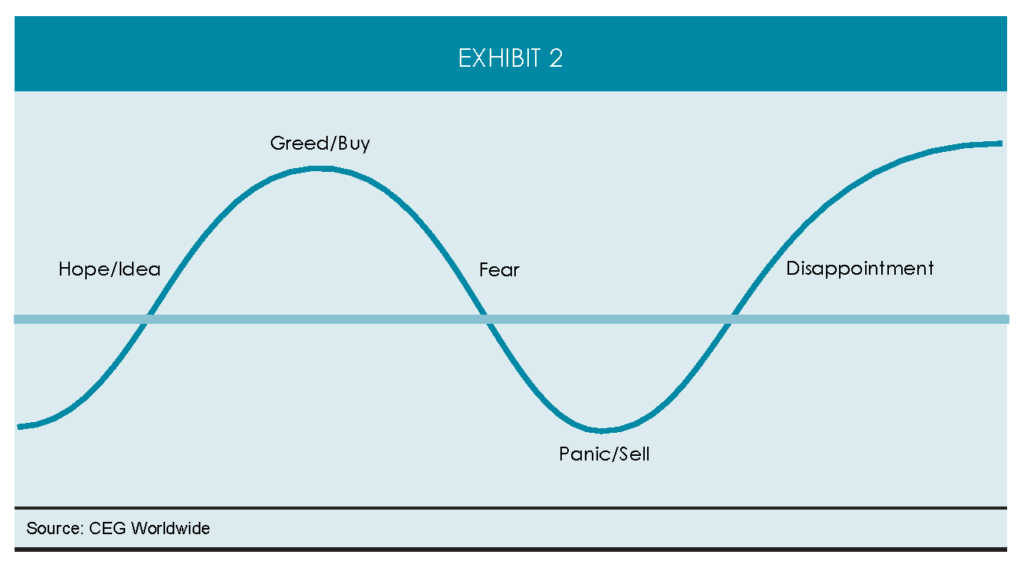

Given the sheer amount of investing noise in today’s world, it’s not surprising that many investors end up making their decisions based on noise. Why do these investors so consistently make the wrong decisions? Because noise drives emotions, and making investment decisions based on emotions rarely has a positive out‐ come. To help you understand the emotions of investing and why most investors systematically make the wrong decisions, let’s look for a moment at what happens when you get a hot tip on a stock.

If you’re like most investors, you don’t buy the stock right away. You’ve probably had the experience of losing money on an investment— and did not enjoy the experience—so you’re not going to race out and buy that stock right away based on a hot tip. You’re cautious, so you decide to follow it for a while to see how it does. Sure enough, it starts trending upward.

You follow it for a while as it rises. What’s your emotion? Confidence. You hope that this might be the one investment that helps you make a lot of money. Let’s say it continues its upward trend. You start feeling a new emotion as you begin to consider that this just might be the one. What is the new emotion? It’s greed. You decide to buy the stock that day.

You know what happens next. Of course, soon after you buy it, the stock starts to go down, and you feel a new combination of emotions—fear and regret. You’re afraid you made a terrible mistake. You promise yourself that if the stock just goes back up to where you bought it, you will never do it again. You don’t want to have to tell your spouse or partner about it. You don’t care about making money anymore.

Now let’s say the stock continues to go down. You find yourself with a new emotion. What is it? It’s panic. You sell the stock. And what happens next? All too often, new information comes out and the stock races to an all‐time high. (See Exhibit 2.)

We’re all poorly wired for investing. Emotions are powerful forces that cause you to do exactly the opposite of what you should do. That is, your emotions lead you to buy high and sell low. If you do that over a long period of time, you’ll cause serious damage not just to your portfolio, but more important, also to your financial dreams.

The good news is that there are superior methods you can use to tune out that noise and build an investment plan that will enable you to achieve consistent investment success. These methods are the ones used by the world’s best institutional money management firms to serve their clients—which include Fortune 500 companies and endowments with billions of dollars to invest. At our firm, we believe that individual investors such as you should have access to the same institutional‐class investment approaches as these companies and endowments enjoy.

As Exhibit 1 shows, there are two institutional-class approaches. The first is the strategic method of making investment decisions. Strategic investors use a process based on Nobel Prize-winning research to build portfolios that provide the best possible returns for a given level of investment risk. Strategic investors rebalance those portfolios on a disciplined quarter‐by‐quarter basis to ensure that they constantly maintain the optimal combination of return and risk.

The second institutional‐class approach is the tactical method. Tactical investors also base their portfolio decisions on Nobel Prize- winning academic research. However, they manage their portfolios differently. Instead of regularly rebalancing each quarter, tactical investors look to add value by emphasizing certain asset classes or market sectors that their research efforts tell them are undervalued and offer an above‐aver‐ age potential for strong returns. Tactical investors then de-emphasize those asset classes or sectors once they become fairly valued by the marketplace. Tactical investors are therefore more opportunistic than strategic investors.

The strategic and tactical approaches are where most of the academic community reside, as do the top institutional investors. Investors who use strategic and tactical investment methods dispassionately research what works and then follow a rational course of action based on empirical evidence. This allows them to ignore the noise created by the media.

Our passion is to help investors make smart decisions about their money. To accomplish this, we help investors move from the noise to making smart decisions about their money by using these prudent investment strategies: 1) strategic investing, 2) tactical investing or 3) a combination of the two approaches. We believe that these strategies will help you maximize the probability of achieving all your financial goals.

Intelligent Investing: Five Key Concepts for Financial Success

© Copyright CEG Worldwide, LLC. All rights reserved.

No part of this publication may be reproduced or retransmitted in any form or by any means, including, but not limited to, electronic, mechanical, photocopying, recording or any information storage retrieval system, without the prior written permission of the publisher. Unauthorized copying may subject violators to criminal penalties as well as liabilities for substantial monetary damages up to $100,000 per infringement, costs and attorneys’ fees.

The information contained herein is accurate to the best of the publisher’s knowledge; however, the publisher can accept no responsibility for the accuracy or completeness of such information or for loss or damage caused by any use thereof.

Click HERE to request a printed copy of this article.